Using Digital Payment Platforms With a Bank Account: Finding the Right Balance

Digital payment apps like Venmo, PayPal, and Cash App have become an easy, everyday way to send and receive money. Fast, convenient, and user-friendly, they’re ideal for splitting a check or paying a friend back.

But when it comes to securely managing your money and building long-term financial stability, these apps aren’t meant to replace your primary checking or savings account.

The smartest approach isn’t choosing one over the other—it’s using each tool for what it does best. Understanding how digital payment platforms and traditional accounts work together can help you protect your funds and manage money more effectively.

What Are Digital Payment Platforms?

Digital payment platforms let you send, receive, and manage money electronically, typically through a mobile app or website. These apps let you link a debit card, credit card, or checking account to pay friends, buy products, or accept payments. For instance, you might pay your share of dinner by sending $25 to a friend via Venmo—no cash or card required. Digital payment platforms are popular because they offer peer-to-peer convenience. But behind the scenes, they’re just a conduit: they rely on linked bank or credit union accounts to fund or withdraw money.

A digital wallet, such as Apple Pay or Google Pay, is another convenient way to make payments. It stores your debit and credit card information securely on your smartphone or tablet, allowing you to make contactless purchases in stores or online. When comparing a digital wallet to a traditional bank account, the key difference is scope. Digital wallets make everyday payments fast and easy, but your checking and savings account offers a full range of tools, protections, and financial management features.

Keeping Digital Payment Platforms in Perspective

While convenient, digital payment platforms aren’t designed to serve as your main financial hub. Some of the biggest drawbacks include:

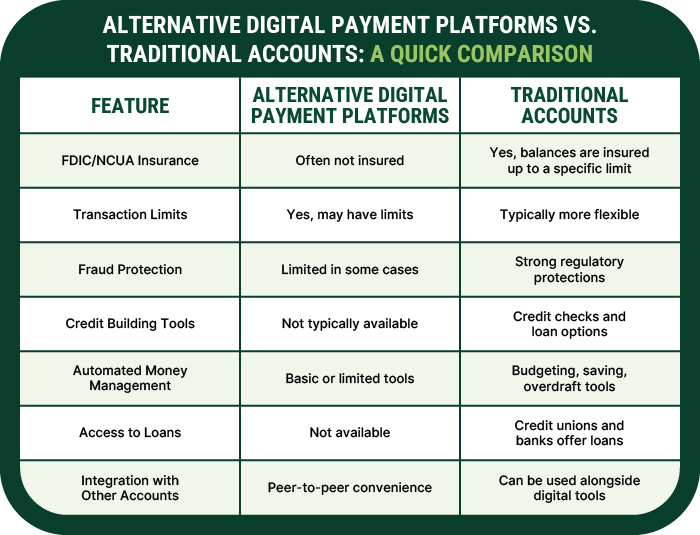

- No account protection. Most platforms aren’t insured by the FDIC (for banks) or NCUA (for credit unions), meaning your money isn’t protected if the company fails or faces fraud or technical problems.

- Transfer limits. You may face caps on how much you can send or withdraw. Transfers to your account often take 1–3 business days.

- Limited fraud protection. If someone gains access to your account, support can be slow or inadequate.

- Few money management tools. These apps don’t support saving goals, credit building, or access to lending products.

A major disadvantage of digital payment platforms is that they’re designed for short-term convenience, not long-term financial management.

Why Traditional Banking Still Matters

Your bank or credit union account is the center of your financial life. It not only provides a safe place to store and grow your money but also offers:

- Essential tools. A traditional account provides checking and savings options, debit cards for everyday use, and access to loans that help you reach short- and long-term financial goals.

- Better money management. Features such as direct deposit, automatic transfers, overdraft protection, and budgeting tools make it easier to organize your finances, pay bills on time, and plan for the future.

- Convenience with coverage. You can still link PayPal, Venmo, or Cash App to your account and use them as intended without sacrificing the safety of insured funds.

- Personal service. Credit unions provide local expertise and real, human support that digital platforms can’t match.

You don’t have to choose between digital convenience and financial security. With a traditional account, you get both.

How Digital Payment Platforms and Traditional Accounts Work Together

It’s not an either/or choice—your digital payment apps and credit union account can work together seamlessly. The safest approach is to use each for what it does best.

Here’s how to get the best of both worlds:

- Secure connection. Link your preferred payment app to your primary account, which serves as the federally insured vault for your money.

- Convenience. Use the app for peer-to-peer payments and purchases.

- Safety. When you receive money, transfer it to your checking or savings account to keep it protected under NCUA insurance.

- Money management. Use your credit union’s tools to save, borrow, and track your money.

By making your primary account your financial foundation, you can access the benefits of both systems.

Alternative Digital Payment Platforms vs. Traditional Accounts: A Quick Comparison

Pair Convenience with Confidence

Digital payment platforms have their place in the modern financial toolkit. But for lasting financial stability, you still need the foundation of a secure, full-service account.

At Heritage Family Credit Union, we make it easy to do both. Our members enjoy powerful online and mobile tools, the ability to link with major payment apps, and access to the full range of financial products and support they need to thrive.

Looking for the right foundation for your money? Open a checking or savings account today and experience the benefits of convenience, coverage, and confidence—all in one place.