Buying a car is a big step, and it can feel even more stressful if you are unsure how to get an auto loan without a long credit history. Many people assume that no credit automatically means no options, but that’s not always the case. With the right preparation and a clear understanding of what lenders look for, it is possible to finance a vehicle and build credit at the same time. This article explains how auto loans work for first-time buyers and borrowers with limited credit, what can improve approval chances, and what obstacles to watch for along the way.

Understanding Credit and Auto Loans

When you apply for a loan, lenders review several factors to decide whether the loan is affordable and sustainable for you. Your credit score for a car loan is one part of that picture, but it is not the only one. A credit score reflects how you have managed borrowed money in the past. If you are new to credit, that history may be thin or nonexistent. In those cases, lenders often look more closely at other details, including:

- Proof of steady income and employment

- Monthly expenses and existing debt obligations

- Whether you have any prior credit activity, even if limited

- The loan amount compared to the value of the vehicle

- Your ability to comfortably manage the monthly payment

Along with reviewing approval factors, seeing how loan details affect affordability can make the process feel more manageable. Loan amount, repayment term, and rate all affect the monthly payment and total cost. A loan calculator allows borrowers to estimate payments and see what amount fits comfortably within their budget.

Getting an Auto Loan With No or Limited Credit

If you’re unsure how to get an auto loan with no credit, showing steady income, keeping payments affordable, and choosing a flexible lender can help. While traditional lenders may rely heavily on credit scores, other financial institutions, like credit unions, may consider additional factors.

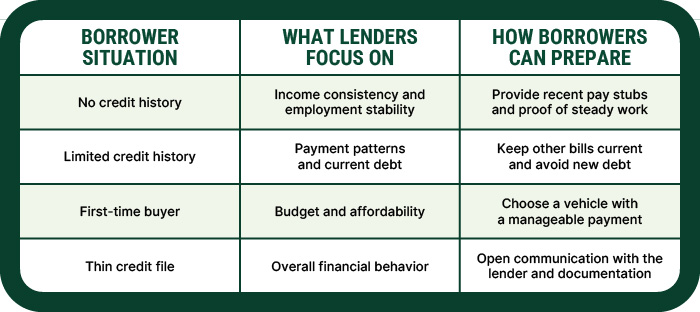

Below is a simple overview of how lenders evaluate different borrower situations.

Borrowers with limited credit history are often approved when income, budget, and payment behavior show consistency. Car loans for no credit are often designed to help borrowers establish a positive payment history, which can support future financial goals.

Steps That Can Improve Approval Chances

Taking a few proactive steps before applying can make a meaningful difference for anyone exploring how to get a car loan with no or limited credit.

- Confirm steady income. Lenders want to see reliable income that supports a consistent monthly payment.

- Save for a down payment. A down payment reduces the amount you need to borrow and can lower overall risk for the lender.

- Review your credit report. Even those with limited credit history should check reports for errors or outdated information.

- Consider a co-signer. A co-signer with established credit who agrees to share responsibility for the loan can strengthen an application.

- Borrow within your budget. Choosing a loan amount that fits comfortably into your monthly expenses improves approval odds and long-term success.

In addition to the monthly payment, it is also important to know the full cost of an auto loan. Some expenses are not always obvious at first glance, and learning about potential hidden costs can help borrowers avoid surprises and make more confident decisions.

Common Factors That Can Prevent Approval

While limited credit does not automatically prevent loan approval, certain issues can make it more difficult. Recognizing these factors helps borrowers prepare more effectively.

- Inconsistent or unverifiable income

- High existing debt compared to income

- Applying for a loan amount that exceeds a realistic budget

- Missing or inaccurate information on the application

Address these issues ahead of time to help improve the application experience.

Why Credit Unions Can Be a Smart Option

Credit unions often take a more personal, relationship-based approach to lending. Rather than focusing solely on a credit score for car loan approval, lenders may consider the full financial picture and take time to understand a borrower’s situation. This can include discussing budget goals, explaining loan terms in plain language, and helping borrowers choose options that support long-term financial stability, not just short-term approval.

Preparing for Long-Term Financial Success

An auto loan is not just a way to purchase a vehicle. It can also be an opportunity to build or strengthen credit over time. Responsible loan management includes:

- Making all payments on time

- Keeping monthly payments affordable and predictable

- Monitoring credit progress as positive history builds

These habits support long-term financial confidence and flexibility.

Successfully navigating how to get an auto loan with limited or no credit starts with education, preparation, and choosing a lender that values the whole person, not just a number. If you’re exploring your options or have questions about auto loans, contact Heritage Family Credit Union. We’re here to help guide you with clear information and personalized support, every step of the way.