What Is GAP Insurance and Why Do You Need It?

No one expects to get into a car accident. But when it happens, the last thing you want to hear is that your vehicle is a total loss. Many drivers assume collision coverage is enough to handle replacement costs. In reality, auto insurance typically pays only the vehicle’s current market value. Because vehicles depreciate quickly, that payout may be less than what you still owe on your auto loan or lease, leaving you responsible for the difference during an already stressful time.

This is where having automobile GAP insurance can make a big difference. This guide explains how it works, what the coverage includes, and when it may be worth considering if you are financing or leasing a vehicle.

What Is Automobile GAP Insurance?

Automobile GAP insurance covers the difference between your car’s actual cash value (ACV) and the remaining balance on your loan or lease after a total loss, such as after an accident or theft. If your insurance settlement does not fully pay off what you owe, this coverage helps close that gap.

GAP coverage is typically offered by a bank, credit union, or dealership when you finance or lease a vehicle, and it is most common with newer vehicles. While it does not replace auto insurance, GAP protection addresses a risk standard policies do not: owing money on a vehicle you can no longer drive.

How Does GAP Insurance Work?

GAP insurance applies after your auto insurer declares a vehicle a total loss and issues an ACV payout. Because that payout is based on market value rather than your loan balance, a difference may remain. GAP insurance helps cover that difference, up to the plan’s limits and subject to exclusions.

Here is how the process typically works:

- A covered event occurs, such as a total loss from an accident or theft.

- Your auto insurer pays the vehicle’s ACV, usually minus the deductible.

- GAP insurance covers some or all of the remaining balance between the payout and what you still owe, within policy limits.

GAP insurance may not pay off every last dollar you owe on your car. The exact amount depends on the specific situation and the terms of your coverage. For example, some plans may not cover certain added costs that get rolled into a loan, and most have limits on how much they will pay.

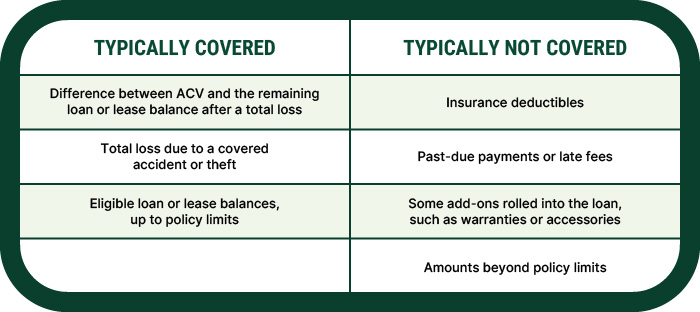

What Does GAP Insurance Cover? (And What it Doesn’t)

If your insurance payout does not fully cover your remaining balance after a total loss, GAP coverage can help reduce or eliminate that difference. However, it is not designed to cover every expense associated with a vehicle.

GAP Insurance Coverage at a Glance

Coverage details vary, so review your GAP addendum carefully to understand exclusions and limits.

Do I Need GAP Insurance if I Have Full Coverage?

Even with full coverage auto insurance, you may still want to consider GAP insurance. Full coverage means you carry both collision and comprehensive, but it does not guarantee that your loan or lease will be paid off after a total loss.

- Collision coverage typically helps pay for damage to your vehicle after an accident involving another vehicle or object, regardless of fault.

- Comprehensive coverage usually helps cover non-collision losses, such as theft, fire, vandalism, or weather-related damage.

Both types of coverage protect the vehicle itself, but not the remaining balance on your loan. GAP insurance addresses that specific financial risk.

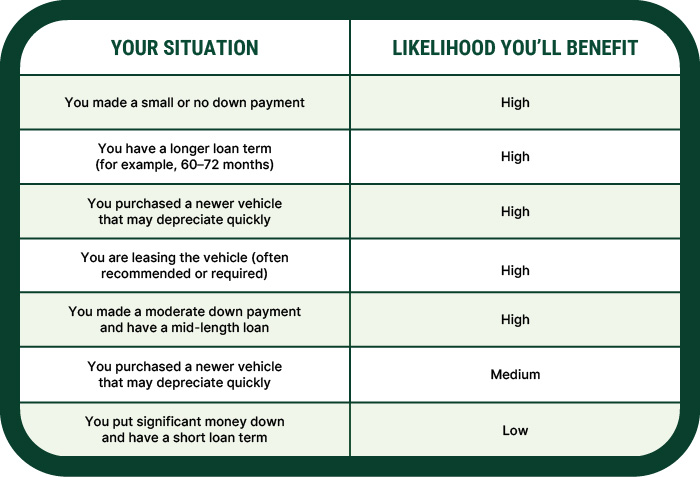

Is GAP Insurance Worth It?

GAP insurance may be worth considering if there is a strong chance your loan balance could exceed your vehicle’s value. Whether or not you need it often depends on factors such as how much you put down, the length of your loan, and how quickly your vehicle depreciates.

Use the rubric below to gauge how likely you are to benefit.

GAP Insurance Benefit Rubric

If several factors fall into the high-likelihood category, insurance with GAP coverage may be worth a closer look. If most fall into the low category, the added protection may be less necessary.

Bring This Checklist To Your Lender

Reviewing these details can help clarify your level of loan balance risk:

- Current payoff amount

- Estimated actual cash value (ACV)

- Down payment amount

- Loan term length

- Whether the vehicle is leased

Can You Add GAP Insurance Later?

In many cases, GAP insurance can be added after financing or leasing a vehicle. However, the most effective time to secure coverage is when you first finance or refinance your vehicle. Adding it early provides coverage during the period when depreciation is typically highest.

If you are considering adding auto insurance GAP protection later, availability may depend on your loan balance, vehicle age, and mileage. Always check with your lender before making changes.

Timing tip: GAP insurance tends to be most beneficial while the risk of negative equity still exists.

If you are exploring auto financing options, Heritage Family Credit Union offers competitively priced GAP options through its auto lending and loan protection resources. Our team is here to help you understand whether automobile GAP insurance fits your situation and your financial goals. If you are financing or refinancing a vehicle, contact us to start the conversation.